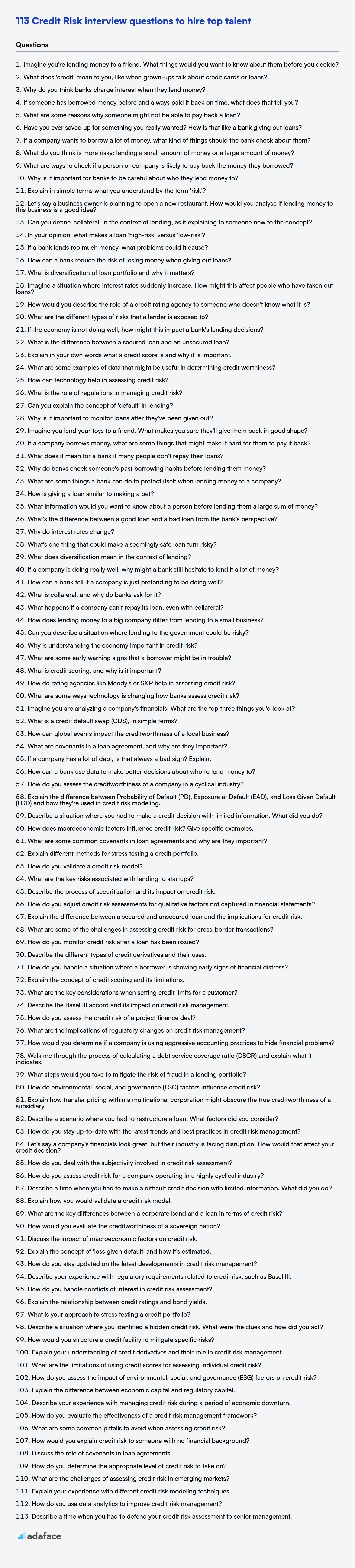

Credit Risk interview questions for freshers

1. Imagine you're lending money to a friend. What things would you want to know about them before you decide?

2. What does 'credit' mean to you, like when grown-ups talk about credit cards or loans?

3. Why do you think banks charge interest when they lend money?

4. If someone has borrowed money before and always paid it back on time, what does that tell you?

5. What are some reasons why someone might not be able to pay back a loan?

6. Have you ever saved up for something you really wanted? How is that like a bank giving out loans?

7. If a company wants to borrow a lot of money, what kind of things should the bank check about them?

8. What do you think is more risky: lending a small amount of money or a large amount of money?

9. What are ways to check if a person or company is likely to pay back the money they borrowed?

10. Why is it important for banks to be careful about who they lend money to?

11. Explain in simple terms what you understand by the term 'risk'?

12. Let's say a business owner is planning to open a new restaurant, How would you analyse if lending money to this business is a good idea?

13. Can you define 'collateral' in the context of lending, as if explaining to someone new to the concept?

14. In your opinion, what makes a loan 'high-risk' versus 'low-risk'?

15. If a bank lends too much money, what problems could it cause?

16. How can a bank reduce the risk of losing money when giving out loans?

17. What is diversification of loan portfolio and why it matters?

18. Imagine a situation where interest rates suddenly increase. How might this affect people who have taken out loans?

19. How would you describe the role of a credit rating agency to someone who doesn't know what it is?

20. What are the different types of risks that a lender is exposed to?

21. If the economy is not doing well, how might this impact a bank's lending decisions?

22. What is the difference between a secured loan and an unsecured loan?

23. Explain in your own words what a credit score is and why it is important.

24. What are some examples of data that might be useful in determining credit worthiness?

25. How can technology help in assessing credit risk?

26. What is the role of regulations in managing credit risk?

27. Can you explain the concept of 'default' in lending?

28. Why is it important to monitor loans after they've been given out?

Credit Risk interview questions for juniors

1. Imagine you lend your toys to a friend. What makes you sure they'll give them back in good shape?

2. If a company borrows money, what are some things that might make it hard for them to pay it back?

3. What does it mean for a bank if many people don't repay their loans?

4. Why do banks check someone's past borrowing habits before lending them money?

5. What are some things a bank can do to protect itself when lending money to a company?

6. How is giving a loan similar to making a bet?

7. What information would you want to know about a person before lending them a large sum of money?

8. What's the difference between a good loan and a bad loan from the bank’s perspective?

9. Why do interest rates change?

10. What's one thing that could make a seemingly safe loan turn risky?

11. What does diversification mean in the context of lending?

12. If a company is doing really well, why might a bank still hesitate to lend it a lot of money?

13. How can a bank tell if a company is just pretending to be doing well?

14. What is collateral, and why do banks ask for it?

15. What happens if a company can't repay its loan, even with collateral?

16. How does lending money to a big company differ from lending to a small business?

17. Can you describe a situation where lending to the government could be risky?

18. Why is understanding the economy important in credit risk?

19. What are some early warning signs that a borrower might be in trouble?

20. What is credit scoring, and why is it important?

21. How do rating agencies like Moody's or S&P help in assessing credit risk?

22. What are some ways technology is changing how banks assess credit risk?

23. Imagine you are analyzing a company's financials. What are the top three things you'd look at?

24. What is a credit default swap (CDS), in simple terms?

25. How can global events impact the creditworthiness of a local business?

26. What are covenants in a loan agreement, and why are they important?

27. If a company has a lot of debt, is that always a bad sign? Explain.

28. How can a bank use data to make better decisions about who to lend money to?

Credit Risk intermediate interview questions

1. How do you assess the creditworthiness of a company in a cyclical industry?

2. Explain the difference between Probability of Default (PD), Exposure at Default (EAD), and Loss Given Default (LGD) and how they're used in credit risk modeling.

3. Describe a situation where you had to make a credit decision with limited information. What did you do?

4. How does macroeconomic factors influence credit risk? Give specific examples.

5. What are some common covenants in loan agreements and why are they important?

6. Explain different methods for stress testing a credit portfolio.

7. How do you validate a credit risk model?

8. What are the key risks associated with lending to startups?

9. Describe the process of securitization and its impact on credit risk.

10. How do you adjust credit risk assessments for qualitative factors not captured in financial statements?

11. Explain the difference between a secured and unsecured loan and the implications for credit risk.

12. What are some of the challenges in assessing credit risk for cross-border transactions?

13. How do you monitor credit risk after a loan has been issued?

14. Describe the different types of credit derivatives and their uses.

15. How do you handle a situation where a borrower is showing early signs of financial distress?

16. Explain the concept of credit scoring and its limitations.

17. What are the key considerations when setting credit limits for a customer?

18. Describe the Basel III accord and its impact on credit risk management.

19. How do you assess the credit risk of a project finance deal?

20. What are the implications of regulatory changes on credit risk management?

21. How would you determine if a company is using aggressive accounting practices to hide financial problems?

22. Walk me through the process of calculating a debt service coverage ratio (DSCR) and explain what it indicates.

23. What steps would you take to mitigate the risk of fraud in a lending portfolio?

24. How do environmental, social, and governance (ESG) factors influence credit risk?

25. Explain how transfer pricing within a multinational corporation might obscure the true creditworthiness of a subsidiary.

26. Describe a scenario where you had to restructure a loan. What factors did you consider?

27. How do you stay up-to-date with the latest trends and best practices in credit risk management?

28. Let’s say a company's financials look great, but their industry is facing disruption. How would that affect your credit decision?

29. How do you deal with the subjectivity involved in credit risk assessment?

Credit Risk interview questions for experienced

1. How do you assess credit risk for a company operating in a highly cyclical industry?

2. Describe a time when you had to make a difficult credit decision with limited information. What did you do?

3. Explain how you would validate a credit risk model.

4. What are the key differences between a corporate bond and a loan in terms of credit risk?

5. How would you evaluate the creditworthiness of a sovereign nation?

6. Discuss the impact of macroeconomic factors on credit risk.

7. Explain the concept of 'loss given default' and how it's estimated.

8. How do you stay updated on the latest developments in credit risk management?

9. Describe your experience with regulatory requirements related to credit risk, such as Basel III.

10. How do you handle conflicts of interest in credit risk assessment?

11. Explain the relationship between credit ratings and bond yields.

12. What is your approach to stress testing a credit portfolio?

13. Describe a situation where you identified a hidden credit risk. What were the clues and how did you act?

14. How would you structure a credit facility to mitigate specific risks?

15. Explain your understanding of credit derivatives and their role in credit risk management.

16. What are the limitations of using credit scores for assessing individual credit risk?

17. How do you assess the impact of environmental, social, and governance (ESG) factors on credit risk?

18. Explain the difference between economic capital and regulatory capital.

19. Describe your experience with managing credit risk during a period of economic downturn.

20. How do you evaluate the effectiveness of a credit risk management framework?

21. What are some common pitfalls to avoid when assessing credit risk?

22. How would you explain credit risk to someone with no financial background?

23. Discuss the role of covenants in loan agreements.

24. How do you determine the appropriate level of credit risk to take on?

25. What are the challenges of assessing credit risk in emerging markets?

26. Explain your experience with different credit risk modeling techniques.

27. How do you use data analytics to improve credit risk management?

28. Describe a time when you had to defend your credit risk assessment to senior management.

Hiring for credit risk roles can be tricky, as it requires a blend of analytical skills and sound judgment; much like hiring for financial analyst roles. To ensure you're selecting the best candidates, it's important to ask the right questions.

This blog post offers a structured collection of credit risk interview questions tailored for various experience levels, from freshers to experienced professionals, including a set of relevant MCQs. These questions aim to help you assess candidates' understanding of credit risk principles, their ability to apply these concepts in real-world scenarios, and their problem-solving aptitude.

Using these questions will help you identify candidates who not only understand credit risk but can also contribute to your organization's success, or you could screen candidates faster, by using our Financial Analyst Test to assess their skills before the interview.

Table of contents

Credit Risk interview questions for freshers

Credit Risk interview questions for juniors

Credit Risk intermediate interview questions

Credit Risk interview questions for experienced

Credit Risk MCQ

Which Credit Risk skills should you evaluate during the interview phase?

Streamline Credit Risk Hiring with Skills Tests and Targeted Interview Questions

Download Credit Risk interview questions template in multiple formats

Credit Risk interview questions for freshers

1. Imagine you're lending money to a friend. What things would you want to know about them before you decide?

Before lending money to a friend, I'd want to understand their financial situation and their reliability. Specifically, I'd consider these factors:

- Reason for the loan: Is it a genuine need or a want? Understanding the purpose helps gauge urgency and responsibility.

- Current income and expenses: Do they have a stable income source? What are their monthly expenses? This helps determine their ability to repay.

- Existing debts: What other financial obligations do they have? Knowing their total debt load is crucial.

- Repayment plan: Do they have a realistic plan for repaying the loan? A proposed schedule with amounts would be ideal.

- Past financial behavior: Have they borrowed money before and repaid it on time? Past behavior is a good predictor of future behavior.

2. What does 'credit' mean to you, like when grown-ups talk about credit cards or loans?

When grown-ups talk about "credit," it's like borrowing money. If you use a credit card, you're borrowing money from the bank to buy something now, and you promise to pay it back later, usually with some extra money (interest) added on top if you don't pay it back quickly. Loans are similar; you borrow a larger amount of money for a longer time, like to buy a house or a car, and you pay it back a little bit each month.

Think of it like this: you're getting something now but agreeing to pay for it later. Having good credit means you're reliable about paying back what you borrow, which makes it easier to borrow money in the future. If you don't pay back what you borrow, it damages your credit and makes it harder to get loans or credit cards later on.

3. Why do you think banks charge interest when they lend money?

Banks charge interest for several reasons. Primarily, it's the cost of the bank foregoing the use of that money themselves; they could be investing it elsewhere. Interest is also compensation for the risk the bank takes that the borrower might not repay the loan. This risk includes factors like the borrower's creditworthiness and the economic climate.

Furthermore, interest covers the bank's operational costs associated with managing the loan, such as processing paperwork, monitoring payments, and dealing with potential defaults. It also contributes to the bank's profit margin, which is necessary for its continued operation and ability to provide financial services.

4. If someone has borrowed money before and always paid it back on time, what does that tell you?

It tells you they have a good credit history. They've demonstrated responsibility and reliability in managing debt. This makes them a lower-risk borrower in the future. Their past behavior indicates a likelihood of fulfilling future loan obligations.

However, it's not the only factor to consider. Other aspects like their current income, employment stability, and overall debt-to-income ratio are also crucial for a comprehensive risk assessment.

5. What are some reasons why someone might not be able to pay back a loan?

There are many reasons why someone might default on a loan. Common causes include job loss or a significant reduction in income, making it difficult to meet regular payments. Unexpected medical expenses or other emergencies can also strain finances and impact repayment ability.

Other contributing factors can be over-indebtedness, where someone has taken on too much debt relative to their income. Changes in interest rates, economic downturns, or poor financial planning can also lead to difficulties in repaying loans. Sometimes, unforeseen circumstances like divorce or natural disasters can also severely impact one's financial situation.

6. Have you ever saved up for something you really wanted? How is that like a bank giving out loans?

Yes, I once saved up for a new laptop. I set a monthly savings goal and put aside a portion of my income until I reached the target amount.

This is similar to a bank giving out loans because both involve delayed gratification and risk assessment. In my case, I delayed immediate spending to gain a larger benefit later. A bank delays receiving the full principal amount by issuing a loan but charges interest as compensation for the risk that the borrower might not repay the loan. Both scenarios depend on the borrower/saver meeting obligations over time to achieve a desired outcome.

7. If a company wants to borrow a lot of money, what kind of things should the bank check about them?

When a company seeks a large loan, a bank will rigorously assess its creditworthiness and ability to repay. Key areas of scrutiny include:

- Financial stability: Analyzing the company's financial statements (balance sheet, income statement, cash flow statement) to assess profitability, liquidity, and solvency. They'll look at key ratios and trends. The bank needs to verify if a company has sufficient current assets against liabilities using quick ratio or current ratio.

- Debt service coverage ratio (DSCR): To see if the company can afford to service the loan.

- Collateral: Evaluating the value and liquidity of assets offered as security for the loan.

- Management team: Assessing the experience and competence of the company's management. Banks will check if the management is capable of taking the company forward.

- Industry outlook: Evaluating the current and future prospects of the industry in which the company operates.

- Market position: Evaluating the competitive landscape and the company's relative standing, like market share.

- Credit history: Checking the company's payment history on previous debts. This will also involve credit rating agencies' assessment of the company. Legal issues are also considered. The bank also considers the intended use of funds and its impact on the company's financial health.

8. What do you think is more risky: lending a small amount of money or a large amount of money?

It depends on the context and risk management strategies. Lending a small amount to many individuals (microloans) can be risky due to the high administrative costs and potential for a higher default rate across a larger pool, despite the small individual loss. The risk is spread, but managing a large number of small loans can be complex.

Conversely, lending a large amount to a single entity carries substantial risk because a default would result in a significant financial loss. However, large loans typically involve more thorough due diligence, collateral, and monitoring, potentially mitigating the risk. The concentration of risk is higher, so the impact of a single failure is greater.

9. What are ways to check if a person or company is likely to pay back the money they borrowed?

Assessing creditworthiness involves evaluating the borrower's ability and willingness to repay. For individuals, this includes checking their credit score (e.g., FICO, VantageScore), reviewing their credit history for past delinquencies or bankruptcies, and analyzing their income and employment stability. Debt-to-income ratio is a crucial metric. Lenders also consider assets and overall financial health. Character references and reputation (though harder to quantify) can play a role too.

For companies, financial statements are key. Analyze their profitability (e.g., net income, EBITDA), liquidity (e.g., current ratio, quick ratio), solvency (e.g., debt-to-equity ratio), and cash flow. Credit ratings from agencies like Moody's or S&P provide an independent assessment. Industry trends and the company's competitive position also impact repayment likelihood. Finally, evaluating management's experience and strategy is important.

10. Why is it important for banks to be careful about who they lend money to?

It's crucial for banks to carefully vet borrowers to mitigate risk and ensure financial stability. Lending to unreliable borrowers increases the likelihood of defaults, meaning the bank won't get its money back. High default rates can erode a bank's profitability and potentially lead to insolvency.

Furthermore, responsible lending practices are vital for maintaining public trust and confidence in the financial system. If banks are perceived as reckless lenders, it can trigger economic instability and harm the overall economy.

11. Explain in simple terms what you understand by the term 'risk'?

Risk, in simple terms, is the possibility of something bad happening. It's the chance that an event will occur that could have a negative impact. This impact could be on anything, like a project, your health, or even your finances. Think of it as the potential for loss or harm.

It's usually described as a combination of two things: the probability of the event happening and the severity of the consequences if it does. So, a low chance of a very bad outcome can still be a significant risk, just as a high chance of a minor inconvenience would also be considered a risk, albeit smaller.

12. Let's say a business owner is planning to open a new restaurant, How would you analyse if lending money to this business is a good idea?

To analyze if lending money to a new restaurant is a good idea, I'd assess several key risk factors. First, I'd evaluate the business plan, including market analysis, competitive landscape, and financial projections (revenue forecasts, cost estimations). I'd focus on the realism and supportability of these projections. Second, I'd scrutinize the owner's experience and expertise in the restaurant industry, and their credit history. Third, I'd analyze the collateral available and the loan's debt service coverage ratio (DSCR). Finally, I'd want to understand the loan's purpose, ensuring it's for a strategic use (like equipment purchase or marketing) and not just covering operational losses.

Specifically, I'd look at factors like:

- Market Demand: Is there sufficient demand for the restaurant's concept in the location?

- Competition: What are the existing restaurants, and what is the new restaurant's competitive advantage?

- Financial Viability: Do the projected financials show a clear path to profitability and positive cash flow?

- Management Team: Does the owner/management team have the experience and skills to operate a successful restaurant?

- Loan Security: What assets can be used as collateral to secure the loan?

If any of these factors indicate high risk, the loan would be considered less desirable.

13. Can you define 'collateral' in the context of lending, as if explaining to someone new to the concept?

Imagine you want to borrow money from a bank. Collateral is something valuable you own that you promise to give to the bank if you can't pay back the loan. It acts as a security for the lender.

Think of it like this: if you borrow money to buy a car, the car itself often serves as collateral. If you fail to make your loan payments, the bank can take the car (repossess it) and sell it to recover their losses. Common examples of collateral include real estate, vehicles, and even investments.

14. In your opinion, what makes a loan 'high-risk' versus 'low-risk'?

A high-risk loan is characterized by a higher probability of default, meaning the borrower is less likely to repay the loan according to the agreed-upon terms. This risk is typically assessed based on factors like the borrower's credit history (low credit score, past defaults), unstable income or employment, high debt-to-income ratio, and insufficient collateral. External factors such as economic downturns or industry-specific risks can also elevate the risk level.

Conversely, a low-risk loan presents a lower probability of default. Borrowers with strong credit scores, stable and sufficient income, low debt-to-income ratios, and adequate collateral are generally considered low-risk. A stable economic environment and a favorable outlook for the borrower's industry also contribute to a lower risk assessment. Essentially, it boils down to the lender's confidence in the borrower's ability and willingness to repay the loan.

15. If a bank lends too much money, what problems could it cause?

If a bank lends too much money, it can lead to several problems. Firstly, it can fuel inflation as more money is circulating in the economy, increasing demand and potentially driving up prices. Secondly, it can increase the risk of defaults on loans. If the bank lends to borrowers who are not creditworthy, or if the economy takes a downturn, many borrowers may struggle to repay their loans, leading to losses for the bank. Finally, excessive lending can create asset bubbles, such as in the housing market, which can eventually burst and cause a financial crisis. Banks can become overleveraged and vulnerable to shocks in the market.

16. How can a bank reduce the risk of losing money when giving out loans?

A bank can reduce the risk of losing money when giving out loans through several strategies. Primarily, they need to rigorously assess the creditworthiness of loan applicants. This involves analyzing their credit history, income, employment stability, and debt-to-income ratio. Stronger financial health indicates a lower risk of default.

Furthermore, the bank can secure the loan with collateral, such as property or assets. This allows the bank to recover some of its losses if the borrower defaults. They can also diversify their loan portfolio across different industries and geographic regions to avoid overexposure to any single sector or economic downturn. Additionally, the bank can implement robust loan monitoring systems to identify early warning signs of potential defaults and take corrective actions promptly. Finally, appropriate pricing of the loan, reflecting the risk associated with the borrower is paramount.

17. What is diversification of loan portfolio and why it matters?

Diversification of a loan portfolio means spreading investments across a variety of loans with different characteristics. These characteristics can include loan type (e.g., mortgage, personal, business), industry, geography, borrower creditworthiness, and loan terms.

It matters because it reduces risk. If all loans are concentrated in one area and that area experiences economic hardship, the entire portfolio suffers. Diversification helps mitigate this by ensuring that losses in one area are offset by gains or stability in others. This leads to a more stable and predictable return on investment.

18. Imagine a situation where interest rates suddenly increase. How might this affect people who have taken out loans?

A sudden increase in interest rates can significantly impact individuals with existing loans. Primarily, their loan repayments will likely increase. This is because many loans, such as variable-rate mortgages or personal loans, are tied to benchmark interest rates. As these rates rise, the interest charged on the loan also increases, leading to higher monthly payments.

This can strain household budgets, potentially leading to financial difficulties. Individuals may have less disposable income for other expenses, and some may struggle to afford their loan repayments, increasing the risk of default. Furthermore, higher interest rates can decrease the affordability of taking out new loans, impacting consumer spending and investment.

19. How would you describe the role of a credit rating agency to someone who doesn't know what it is?

Imagine you want to borrow money, like a company issuing bonds to fund a project. A credit rating agency is like a financial report card. They analyze the company's financial health and assign a rating, like AAA (very safe) or B (risky). This rating tells investors how likely the company is to repay its debt.

Essentially, these agencies provide an independent assessment of creditworthiness. This helps investors make informed decisions about where to put their money. A higher rating means lower risk, and usually, a lower interest rate for the borrower. Conversely, a lower rating signals higher risk and potentially higher interest rates. It's like a score that measures the risk of lending money to a particular entity.

20. What are the different types of risks that a lender is exposed to?

Lenders face several key risks. Credit risk is the most prominent, referring to the possibility that a borrower will default on their debt obligations. Liquidity risk arises when a lender cannot meet its own obligations because of difficulty converting assets to cash. Interest rate risk impacts lenders when changes in interest rates reduce the value of their assets or increase their borrowing costs. Other risks include operational risk (failures in internal processes, people, and systems), market risk (changes in market conditions affecting asset values), and regulatory risk (adverse changes in laws or regulations).

21. If the economy is not doing well, how might this impact a bank's lending decisions?

If the economy is struggling, banks typically become more cautious with their lending. They face increased risk of borrowers defaulting on loans due to job losses or business closures. This leads banks to tighten their lending criteria, requiring higher credit scores, larger down payments, and more collateral.

Consequently, banks may reduce the overall volume of loans they issue, focusing on lower-risk borrowers and industries. They might also increase interest rates to compensate for the heightened risk. This contraction in lending can further dampen economic activity, creating a feedback loop.

22. What is the difference between a secured loan and an unsecured loan?

The main difference between a secured and unsecured loan lies in whether or not the loan is backed by collateral. A secured loan is backed by an asset (like a house or car), which the lender can seize if the borrower defaults on the loan. This reduces the lender's risk. Examples include mortgages and auto loans.

An unsecured loan, on the other hand, isn't backed by any collateral. Because of the higher risk to the lender, these loans typically have higher interest rates. Common examples are credit cards, personal loans, and student loans.

23. Explain in your own words what a credit score is and why it is important.

A credit score is a three-digit number that summarizes your creditworthiness. It's based on your credit history, including how often you've borrowed money and how reliably you've repaid it. Lenders use it to assess the risk of lending you money. A higher score means you're seen as a lower risk.

It's important because it affects whether you're approved for loans (like mortgages, car loans, and credit cards) and the interest rates you'll receive. A good credit score can save you significant money over time, as you'll qualify for better terms. It can also impact things like renting an apartment, getting insurance, and even some job opportunities.

24. What are some examples of data that might be useful in determining credit worthiness?

Several categories of data are useful for determining creditworthiness. Payment history, including on-time payments for credit cards, loans, and mortgages, is a primary indicator. The amount of outstanding debt relative to available credit, often expressed as a credit utilization ratio, is also crucial. Length of credit history provides insights into responsible credit management over time. Types of credit used (e.g., installment loans, revolving credit) and any instances of bankruptcy or other adverse public records are also considered.

Income and employment stability provide an indication of the ability to repay debts. Information from credit bureaus, such as credit scores (e.g., FICO, VantageScore), summarizes much of this data into a single, easily digestible number. Additional data like rent payments and utility bill payments, while not traditionally included in credit reports, are increasingly being used to supplement creditworthiness assessments, especially for individuals with limited credit history.

25. How can technology help in assessing credit risk?

Technology significantly enhances credit risk assessment through various means. Machine learning models can analyze vast datasets, including credit history, transaction data, and alternative data sources (social media activity, online behavior), to predict creditworthiness more accurately than traditional methods. Automated systems streamline the application process, reducing manual errors and processing time.

Specifically, technology enables:

- Improved data collection and analysis: Accessing and analyzing diverse data points (bank statements, utility bills, online sales data) for a holistic view.

- Automated scoring models: Developing predictive models using algorithms to assess risk based on numerous variables.

- Fraud detection: Identifying suspicious patterns and fraudulent activities to prevent losses. Real-time monitoring of transactions can flag anomalies instantly.

- Enhanced reporting and compliance: Generating automated reports for regulatory compliance and internal risk management.

26. What is the role of regulations in managing credit risk?

Regulations play a crucial role in managing credit risk by establishing standards and guidelines that financial institutions must follow. These regulations aim to ensure that institutions adequately assess, monitor, and control their credit exposures. Key aspects include setting minimum capital requirements to absorb potential losses, defining acceptable risk management practices for loan origination and portfolio management, and mandating transparent reporting of credit risk exposures. Basel III, for example, provides an international regulatory framework for bank capital adequacy, stress testing, and liquidity risk management.

Furthermore, regulations often require banks to classify assets based on risk and maintain adequate provisions for potential loan losses. They also influence credit rating agencies, promoting greater accuracy and independence in their assessments. By enforcing these measures, regulations help to maintain the stability of the financial system, protect depositors, and prevent excessive risk-taking that could lead to financial crises. Dodd-Frank Act in the US is another example of regulations aimed at reducing systemic risk in the financial system.

27. Can you explain the concept of 'default' in lending?

In lending, 'default' generally refers to a borrower's failure to repay a debt according to the agreed-upon terms. This typically means missing payments for a specified period, violating loan covenants, or otherwise breaching the loan agreement. Default is a serious situation with significant consequences for both the borrower (credit score damage, potential asset seizure) and the lender (financial loss).

28. Why is it important to monitor loans after they've been given out?

Monitoring loans after disbursement is crucial for several reasons. Primarily, it allows lenders to identify potential issues early, such as borrowers struggling to make payments or experiencing financial difficulties. Early detection enables proactive intervention, like offering modified payment plans or financial counseling, increasing the likelihood of loan repayment and minimizing losses.

Furthermore, monitoring helps assess the overall health of the loan portfolio. It provides valuable data on loan performance, risk exposure, and the effectiveness of lending policies. This information is essential for making informed decisions about future lending practices, risk management strategies, and regulatory compliance. It helps to ensure the long term sustainability of the lending institution.

Credit Risk interview questions for juniors

1. Imagine you lend your toys to a friend. What makes you sure they'll give them back in good shape?

Trust is a big part of it. I'd lend my toys to a friend I trust to respect my things. I might also set some ground rules beforehand, like asking them to be careful or only use them in a certain way. Clear communication about expectations is key. To increase the chance of getting them back as they were, I might only lend toys that aren't my absolute favorites or ones that are easily replaceable. This reduces anxiety if something happens to them.

Beyond that, sometimes a little bit of hope and faith is necessary. While it's important to be proactive, you can't 100% guarantee anything, so I’d manage my expectations to some extent.

2. If a company borrows money, what are some things that might make it hard for them to pay it back?

Several factors can hinder a company's ability to repay borrowed money. A significant decrease in revenue due to market changes, increased competition, or a general economic downturn can strain cash flow. Unexpected expenses, such as legal settlements, equipment failures, or raw material price spikes, can also deplete resources. Poor financial management, including overspending, inefficient operations, or inadequate budgeting, can lead to liquidity problems.

Further complicating matters, high interest rates on the loan itself increase the repayment burden. Restrictive loan covenants, like limitations on capital expenditures or dividend payments, can limit financial flexibility. Finally, inaccurate financial forecasting or a failure to adapt to changing business conditions can result in an inability to meet debt obligations.

3. What does it mean for a bank if many people don't repay their loans?

If a significant number of people fail to repay their loans, it has severe consequences for the bank. Primarily, it leads to a reduction in the bank's assets and profitability, as the loans become non-performing assets. This can erode the bank's capital base, potentially leading to financial instability.

Specifically, the bank faces potential liquidity issues (difficulty meeting obligations), decreased lending capacity (can't lend as much), and reputational damage. In extreme scenarios, widespread loan defaults can even trigger a bank run, where depositors rush to withdraw their funds, or, in the worst case, bank failure. Increased non-performing loans often lead to stricter lending criteria in the future.

4. Why do banks check someone's past borrowing habits before lending them money?

Banks check someone's past borrowing habits, typically through credit reports and scores, to assess the risk of lending to that individual. A history of responsible borrowing, like consistently paying bills on time and managing debt effectively, indicates a lower risk. Conversely, a history of late payments, defaults, or high debt levels suggests a higher risk that the borrower may struggle to repay the loan.

By analyzing past borrowing behavior, banks can make informed decisions about whether to approve a loan, what interest rate to charge, and what loan terms to offer. This process helps them minimize potential losses and maintain the stability of their lending portfolio.

5. What are some things a bank can do to protect itself when lending money to a company?

When lending money to a company, a bank can take several steps to mitigate risk. Firstly, the bank can secure the loan with collateral, meaning if the company defaults, the bank can seize and sell the asset to recover funds. This can include property, equipment, or accounts receivable. Secondly, banks perform thorough due diligence, analyzing the company's financial statements, business plan, and market position to assess its ability to repay the loan. They also look into the company's management team and their track record.

Thirdly, the bank can implement loan covenants, which are conditions the company must adhere to during the loan term. These may include maintaining certain financial ratios, limiting dividend payouts, or restricting further borrowing. Regular monitoring of the company's performance and compliance with these covenants allows the bank to identify potential problems early. Finally, the bank may require a personal guarantee from the company's owner or another entity, making them personally liable for the debt if the company defaults.

6. How is giving a loan similar to making a bet?

Giving a loan is similar to making a bet because in both scenarios, you're wagering on a future outcome. In lending, you're betting that the borrower will repay the principal plus interest, essentially betting on their ability to manage their finances and generate sufficient income. There's inherent risk involved, as the borrower might default, similar to losing a bet if the predicted outcome doesn't materialize.

Both also involve assessing risk and potential reward. Lenders evaluate creditworthiness, financial stability, and market conditions to determine the likelihood of repayment, just as a gambler assesses the odds and potential payout before placing a bet. A higher perceived risk typically leads to a higher interest rate on the loan (a larger potential reward for the lender) or less favorable terms, mirroring how higher-risk bets often offer larger payouts.

7. What information would you want to know about a person before lending them a large sum of money?

Before lending a large sum of money, I'd want to know a person's credit history (including credit score and any past defaults), their current income and employment status, their debt-to-income ratio, and their assets and liabilities. Understanding their financial stability and repayment capacity is crucial.

I'd also want to understand the purpose of the loan and their proposed repayment plan. A well-defined plan increases the likelihood of repayment. Finally, I'd perform due diligence by verifying the information provided through independent sources where possible.

8. What's the difference between a good loan and a bad loan from the bank’s perspective?

From a bank's perspective, a good loan is one that is likely to be repaid fully and on time, generating profit (interest) with minimal risk. These loans are typically backed by sufficient collateral, have a low debt-to-income ratio for the borrower, and show a strong credit history.

A bad loan, conversely, carries a high risk of default. This might involve borrowers with poor credit scores, unstable income, or insufficient collateral to cover the loan amount. Bad loans can result in financial losses for the bank due to unpaid principal and interest, and also increase the bank's regulatory capital requirements.

9. Why do interest rates change?

Interest rates change primarily due to shifts in the supply and demand for money. When demand for borrowing increases (perhaps due to economic expansion), interest rates tend to rise. Conversely, when there's an excess of money available for lending, interest rates may fall.

Central banks also play a significant role by adjusting benchmark interest rates to manage inflation and stimulate or cool down the economy. They might lower rates to encourage borrowing and spending during a recession or raise rates to combat rising prices.

10. What's one thing that could make a seemingly safe loan turn risky?

One key factor that can transform a seemingly safe loan into a risky one is a significant change in the borrower's financial situation or the overall economic environment. For example, job loss, unexpected major expenses (medical bills, natural disasters), or a sharp downturn in the economy can drastically reduce a borrower's ability to repay the loan.

Another contributing element is a drastic change in the value of collateral. If the loan is secured by an asset, such as a house, a sudden decrease in the asset's market value can leave the lender with insufficient recourse in case of default. This is particularly relevant in real estate or rapidly depreciating asset markets.

11. What does diversification mean in the context of lending?

In lending, diversification refers to spreading credit risk across a variety of borrowers, industries, geographies, and loan types. The goal is to reduce the lender's overall exposure to any single borrower or event that could lead to significant losses. By not putting all eggs in one basket, a lender can mitigate the impact of defaults from a particular segment of their portfolio.

Diversification can be achieved through various methods, such as setting limits on the concentration of loans to a single borrower or industry, targeting different geographic regions, and offering diverse loan products with varying risk profiles. This strategy aims to improve the stability and resilience of the lender's loan portfolio against economic downturns or unforeseen circumstances.

12. If a company is doing really well, why might a bank still hesitate to lend it a lot of money?

Even a successful company can present risks that make a bank cautious about lending large sums. A primary concern is over-leveraging. The bank needs to assess whether the company's success is sustainable and if it can comfortably manage significantly higher debt levels, especially if the industry is cyclical or sensitive to economic downturns. A large loan could strain the company's cash flow if profitability decreases.

Another factor is the concentration of risk. If the company's success relies heavily on a few key customers or products, the bank might hesitate due to the potential impact of losing one of those key elements. Furthermore, the bank will meticulously examine the company's financial statements and projections, assessing the quality of earnings and ensuring that reported profits are not artificially inflated or unsustainable. They will also want to see how the cash flow would be affected by a large expenditure or the impact on other loans.

13. How can a bank tell if a company is just pretending to be doing well?

Banks employ several strategies to identify companies that are falsely portraying financial health. They scrutinize financial statements for inconsistencies, such as unusual revenue recognition patterns, inflated asset valuations, or discrepancies between reported profits and actual cash flow. Banks may also conduct independent audits and verify information with third parties like suppliers and customers. Key ratios like debt-to-equity, current ratio, and profitability margins are closely monitored for deviations from industry norms or historical trends.

Beyond financials, banks assess the company's operational and market environment. A sudden change in market share, customer churn, or increased reliance on short-term debt can signal underlying problems. Banks also pay attention to management's track record, industry reputation, and internal controls. Red flags include frequent changes in accounting firms, aggressive accounting practices, or a lack of transparency in financial reporting.

14. What is collateral, and why do banks ask for it?

Collateral is an asset that a borrower offers to a lender to secure a loan. It acts as a guarantee for the lender; if the borrower defaults on the loan payments, the lender can seize the collateral and sell it to recover the outstanding debt. Examples include real estate, vehicles, or investments.

Banks ask for collateral to mitigate their risk. Lending money always involves the risk that the borrower won't repay. By requiring collateral, banks reduce their potential losses if a borrower defaults. The collateral provides them with a tangible asset that they can liquidate to recoup their funds. This makes them more willing to provide loans, especially to borrowers who may be seen as higher risk.

15. What happens if a company can't repay its loan, even with collateral?

If a company defaults on a loan even after the collateral is seized and sold, it indicates that the proceeds from the collateral sale were insufficient to cover the outstanding loan amount. This situation leads to a deficiency. The lender then becomes an unsecured creditor for the remaining deficiency amount.

The lender can pursue legal action to recover the remaining debt. This might involve attempting to seize other company assets, garnishing wages (if applicable), or pursuing a judgment against the company. The company might be forced into bankruptcy proceedings (either Chapter 7 liquidation or Chapter 11 reorganization) if it cannot meet its financial obligations. In bankruptcy, other creditors also make claims, and assets are distributed according to the established priority rules.

16. How does lending money to a big company differ from lending to a small business?

Lending to a large company differs significantly from lending to a small business primarily due to scale, risk assessment, and available resources. Large companies generally have established credit histories, audited financial statements, and diverse revenue streams, making risk assessment more predictable. They often have access to diverse funding options like bond markets, enabling them to borrow at potentially lower interest rates.

Small businesses, on the other hand, usually lack the extensive financial history and resources of larger firms. Their creditworthiness assessment relies more heavily on the owner's credit score and business plan. Due to higher perceived risk, small business loans often come with higher interest rates and may require personal guarantees or collateral. The loan process tends to be more relationship-based with local banks or credit unions.

17. Can you describe a situation where lending to the government could be risky?

Lending to a government can be risky if the government's fiscal situation deteriorates significantly. This could arise from factors such as economic recession leading to decreased tax revenues, unsustainable spending policies, or a sharp increase in national debt. A government facing a debt crisis might resort to measures that harm lenders, such as defaulting on its debt obligations, restructuring debt with unfavorable terms, or inflating away the real value of the debt through excessive money printing.

Another risk arises from political instability. A change in government could lead to a repudiation of existing debts or a shift in economic policy that makes it more difficult for the government to repay its obligations. Furthermore, geopolitical events like wars or sanctions can severely impact a government's ability to manage its finances and service its debt, increasing the risk for lenders.

18. Why is understanding the economy important in credit risk?

Understanding the economy is crucial in credit risk because economic conditions directly impact borrowers' ability to repay their debts. A strong economy typically leads to lower unemployment and increased consumer spending, making it easier for individuals and businesses to meet their financial obligations. Conversely, an economic downturn can result in job losses, reduced income, and decreased profitability, increasing the likelihood of defaults.

Credit risk models often incorporate macroeconomic indicators, such as GDP growth, interest rates, and inflation, to assess the probability of default. By monitoring these economic factors, credit risk professionals can proactively identify and manage potential risks in their portfolios, adjusting lending policies and risk mitigation strategies as needed. Ignoring the economy can lead to significant losses, as unforeseen economic shocks can rapidly deteriorate credit quality across various sectors.

19. What are some early warning signs that a borrower might be in trouble?

Several early warning signs can indicate a borrower is facing financial difficulties. These can be broadly categorized into behavioral and financial indicators. Keep an eye out for:

- Delayed Payments: Consistently late or missed payments are a primary indicator.

- Increased Credit Utilization: Maxing out credit cards or using a significant portion of available credit.

- Changes in Communication: Avoiding contact, providing inconsistent information, or becoming defensive when questioned about finances.

- Frequent Overdrafts/NSF Fees: Bouncing checks or repeatedly overdrawing bank accounts.

- Unexplained Changes in Spending Habits: Sudden decrease in spending or significantly different spending patterns than normal.

- Taking out Multiple New Loans: Applying for or obtaining numerous loans in a short period can signify a need for cash.

- Negative News: News about the borrower, the industry they work in, or the company they work for.

20. What is credit scoring, and why is it important?

Credit scoring is a statistical analysis performed by lenders and financial institutions to determine the creditworthiness of an individual or business. It assigns a numerical score based on an applicant's credit history, financial situation, and other relevant factors, predicting the likelihood they will repay a debt.

Credit scoring is important because it helps lenders make informed decisions about extending credit, managing risk, and setting interest rates. For individuals, a good credit score can lead to better loan terms, lower interest rates, and easier access to credit, affecting their ability to purchase homes, cars, and other significant assets. It can also impact things like insurance premiums and rental applications.

21. How do rating agencies like Moody's or S&P help in assessing credit risk?

Rating agencies like Moody's and S&P assess credit risk by assigning ratings to debt instruments (e.g., bonds) and issuers. These ratings indicate the agency's opinion on the likelihood of the issuer's ability to repay its debt obligations. Higher ratings (e.g., AAA) signify lower credit risk and a higher probability of repayment, while lower ratings (e.g., CCC or below) suggest higher credit risk and a greater chance of default. These ratings help investors and other market participants quickly gauge the creditworthiness of borrowers and make informed investment decisions.

Essentially, they provide a standardized and readily available measure of credit risk that would otherwise require significant due diligence and expertise to determine independently. This standardization enables easier comparison of different debt instruments and facilitates efficient capital allocation.

22. What are some ways technology is changing how banks assess credit risk?

Technology is revolutionizing credit risk assessment in banking through enhanced data analysis and automation. Banks are increasingly leveraging big data analytics, machine learning, and AI to analyze vast datasets, including credit history, transaction data, social media activity, and alternative data sources, to identify patterns and predict creditworthiness more accurately. This allows for more nuanced risk profiling than traditional methods.

Specifically, technologies such as automated underwriting systems expedite loan approvals while maintaining accuracy. Furthermore, banks utilize real-time monitoring systems powered by AI to detect early warning signs of financial distress in borrowers, allowing for proactive risk mitigation strategies. Open Banking initiatives also play a role by securely providing access to customer-permissioned data, offering a more holistic view of a borrower's financial situation.

23. Imagine you are analyzing a company's financials. What are the top three things you'd look at?

If I were analyzing a company's financials, I'd focus on three key areas:

Revenue Growth & Profitability: I'd look at the trend in revenue growth, comparing it to industry averages and competitors. Critically, I'd examine profitability metrics like gross margin, operating margin, and net profit margin. Are these margins improving, stable, or declining? Understanding the relationship between revenue and profitability is crucial for assessing a company's efficiency and competitive advantage.

Cash Flow: I'd analyze the company's cash flow statement, paying particular attention to cash flow from operations. Is the company generating sufficient cash from its core business to fund its operations, investments, and debt repayments? Free cash flow (FCF) is also important to calculate, as it indicates cash available to the company after all expenses are paid.

Debt & Liquidity: I would assess the company's debt levels and liquidity ratios. High debt levels can be risky, especially in a challenging economic environment. Liquidity ratios, such as the current ratio and quick ratio, indicate the company's ability to meet its short-term obligations. A healthy balance sheet with manageable debt and adequate liquidity is a sign of financial stability.

24. What is a credit default swap (CDS), in simple terms?

A Credit Default Swap (CDS) is like an insurance policy for lenders. If a borrower defaults on a loan or bond, the CDS seller compensates the buyer for the loss. The buyer makes periodic payments (like insurance premiums) to the seller for this protection.

Think of it this way: I lend money to company X. I'm worried they might go bankrupt. So, I buy a CDS from company Y. If company X does go bankrupt, company Y pays me the money I lost. If company X doesn't go bankrupt, I just keep paying company Y the regular 'premium' for the CDS contract.

25. How can global events impact the creditworthiness of a local business?

Global events can significantly impact the creditworthiness of a local business through several channels. Supply chain disruptions (e.g., due to geopolitical instability or pandemics) can increase input costs and delay production, leading to decreased revenue and difficulty in meeting financial obligations. Changes in global demand can also affect a local business's sales, especially if it exports goods or services or relies on international tourism.

Furthermore, global economic downturns can reduce consumer spending and investment, impacting even businesses focused solely on local markets. Increased inflation, often a result of global events, can erode purchasing power and increase operating costs, making it harder for the business to manage its debt and maintain a positive credit rating. Interest rate hikes, implemented to combat inflation, further strain the business's ability to borrow and repay loans.

26. What are covenants in a loan agreement, and why are they important?

Covenants in a loan agreement are promises or agreements made by the borrower to the lender. They are designed to protect the lender's investment by ensuring the borrower maintains financial health and operates responsibly. Covenants can be affirmative (requiring the borrower to do something, like maintain insurance) or negative (restricting the borrower from doing something, like taking on additional debt).

The importance of covenants lies in their ability to provide early warning signs of potential financial distress and offer the lender recourse if the borrower violates the agreed-upon terms. They allow lenders to proactively manage risk rather than reactively dealing with a default. Breaching a covenant can trigger various remedies for the lender, including demanding immediate repayment of the loan.

27. If a company has a lot of debt, is that always a bad sign? Explain.

No, a company having a lot of debt is not always a bad sign. It depends on several factors. Debt can be a tool for growth if used strategically. For example, a company might take on debt to invest in new projects, expand operations, or acquire other businesses. If these investments generate returns that exceed the cost of the debt, it can increase profitability and shareholder value.

However, high debt levels can become problematic if the company struggles to manage its debt obligations, especially if interest rates rise or if the company's revenues decline. Excessive debt can lead to financial distress, reduced flexibility, and even bankruptcy. Therefore, it's important to consider the context, including the company's industry, profitability, cash flow, and overall financial health, to determine if the level of debt is appropriate.

28. How can a bank use data to make better decisions about who to lend money to?

Banks can leverage data to enhance their lending decisions by analyzing various factors to predict creditworthiness. This involves building predictive models using historical loan data, credit scores, transaction history, and demographic information. They can identify patterns and correlations between these factors and loan defaults, enabling them to assess risk more accurately.

Specifically, a bank might use machine learning algorithms to build a model that estimates the probability of default. Input features could include:

- Credit Score: Experian, Equifax, TransUnion scores.

- Income: Verified income from pay stubs or tax returns.

- Debt-to-Income Ratio (DTI): Total debt divided by gross monthly income.

- Employment History: Length of employment and job stability.

- Loan Amount and Purpose: Size of the loan and intended use.

By carefully evaluating these data points and using sophisticated analytical techniques, banks can make more informed decisions about loan approvals, interest rates, and loan terms, ultimately reducing the risk of defaults and improving profitability.

Credit Risk intermediate interview questions

1. How do you assess the creditworthiness of a company in a cyclical industry?

Assessing creditworthiness in a cyclical industry requires a focus on long-term viability and resilience. I'd look beyond recent performance, focusing on factors that indicate a company's ability to weather downturns. Key metrics include analyzing the company's cash flow generation throughout multiple economic cycles, maintaining a conservative capital structure with low debt levels, and assessing management's experience in navigating previous downturns.

Furthermore, I would evaluate the company's competitive position, cost structure, and diversification. A company with a strong market share, efficient operations, and diverse revenue streams is better positioned to withstand industry fluctuations. Stress testing the company's financial model under various recessionary scenarios is also crucial to determine its sensitivity to economic downturns and its ability to meet its financial obligations even in adverse conditions.

2. Explain the difference between Probability of Default (PD), Exposure at Default (EAD), and Loss Given Default (LGD) and how they're used in credit risk modeling.

Probability of Default (PD) is the likelihood that a borrower will be unable to meet their debt obligations within a specific time horizon (usually one year). Exposure at Default (EAD) represents the estimated outstanding amount a lender is exposed to at the time a borrower defaults. Loss Given Default (LGD) is the percentage of the EAD that the lender expects to lose after recovering what they can from the defaulted exposure.

In credit risk modeling, these three components are crucial for calculating expected loss (EL). The formula is: EL = PD * EAD * LGD. PD provides the probability of the default event, EAD quantifies the amount at risk, and LGD estimates the severity of the loss should default occur. Credit risk models use these values to determine capital reserves, set interest rates, and manage overall portfolio risk.

3. Describe a situation where you had to make a credit decision with limited information. What did you do?

In a prior role, I had to approve credit limits for new small business customers with limited credit history. To address this, I relied heavily on the information I could gather from alternative sources. This included reviewing bank statements provided by the applicant to assess cash flow, analyzing the industry they operated in for typical revenue patterns and risks, and verifying their business registration and online presence for legitimacy.

Ultimately, I made a conservative decision, granting a lower initial credit limit than requested for risk mitigation purposes. I communicated to the customer that their limit would be reviewed and potentially increased after a successful repayment period, incentivizing responsible credit behavior and allowing us to reassess their risk profile with more concrete data.

4. How does macroeconomic factors influence credit risk? Give specific examples.

Macroeconomic factors significantly impact credit risk by influencing borrowers' ability and willingness to repay debts. Economic downturns, characterized by decreased GDP growth and increased unemployment, directly impair borrowers' incomes and cash flows, leading to higher default rates across various loan types, from mortgages to corporate bonds. Rising interest rates, often a tool to combat inflation, increase borrowing costs for both individuals and businesses, making it more difficult to service existing debt and discouraging new investments, thus elevating credit risk.

Specific examples include: A recession causing widespread job losses, increasing mortgage defaults; High inflation eroding purchasing power, leading to more credit card defaults; Changes in housing market conditions affecting the value of collateral, impacting loan-to-value ratios and increasing risks for lenders; Government policies, like changes in tax laws, affecting disposable income and business profitability.

5. What are some common covenants in loan agreements and why are they important?

Common loan covenants are promises made by the borrower to the lender. They're important because they help the lender monitor the borrower's financial health and reduce the risk of default.

Some common types include:

- Financial covenants: These relate to the borrower's financial performance, like maintaining a certain debt-to-equity ratio or a minimum level of working capital.

- Affirmative covenants: These are things the borrower must do, such as providing regular financial statements or maintaining insurance.

- Negative covenants: These are things the borrower cannot do without the lender's permission, such as taking on additional debt or selling significant assets. These covenants give the lender early warning signs and allow them to take action if the borrower's financial situation deteriorates, protecting the lender's investment.

6. Explain different methods for stress testing a credit portfolio.

Stress testing a credit portfolio involves simulating adverse economic scenarios to assess potential losses. Several methods exist: Scenario analysis involves defining specific hypothetical events (e.g., recession, interest rate shock) and estimating their impact on borrowers' ability to repay loans. Sensitivity analysis tests the portfolio's resilience to changes in key parameters like default probabilities or loss given default, one at a time. Reverse stress testing identifies scenarios that would cause the portfolio to fail, helping to understand vulnerabilities. Finally, Factor-based stress testing uses statistical models to estimate the impact of macroeconomic factors on credit risk. These methods can be implemented using historical data, statistical models, and expert judgment.

The choice of method depends on data availability, model complexity, and regulatory requirements. Scenario analysis and sensitivity analysis are relatively simple to implement, while reverse stress testing and factor-based models require more sophisticated techniques. It's common practice to combine multiple methods for a comprehensive assessment.

7. How do you validate a credit risk model?

Validating a credit risk model involves several key steps. First, assess the model's discriminatory power using metrics like the Gini coefficient, AUC (Area Under the Curve), or KS statistic. These measures quantify the model's ability to distinguish between good and bad credit risks. Second, evaluate the model's calibration, which determines how well the predicted probabilities align with actual default rates. Techniques like calibration plots or the Hosmer-Lemeshow test can be used. Finally, perform out-of-time and out-of-sample testing to ensure the model's performance generalizes to unseen data and across different time periods, checking for model drift. Stress-testing using extreme scenarios can help understand model limitations and potential vulnerabilities.

Furthermore, backtesting can be used to compare the model's predictions to historical outcomes. Monitoring key performance indicators (KPIs) over time helps identify any degradation in model performance. Model validation should also include documentation review, process validation, and independent reviews to ensure data quality, model assumptions, and overall model governance. These steps are crucial to ensure the stability and reliability of the credit risk model over time.

8. What are the key risks associated with lending to startups?

Lending to startups carries significant risks due to their inherent instability. Key risks include: High Failure Rate: Startups have a high probability of failure, leading to potential loss of the principal. Limited or No Operating History: Lack of historical financial data makes it difficult to assess creditworthiness. Unproven Business Model: The startup's business model might not be viable or scalable. Liquidity Risk: Startups often have limited cash reserves and can face difficulty meeting debt obligations. Market Volatility: Startups are highly susceptible to changes in market conditions and competitive pressures. Management Team Inexperience: Inexperienced management teams can make poor strategic decisions. Collateral Limitations: Startups may have limited tangible assets to offer as collateral.

Mitigation strategies often involve higher interest rates to compensate for the risk, equity kickers to share in potential upside, shorter loan terms, and stringent covenants to monitor performance closely.

9. Describe the process of securitization and its impact on credit risk.

Securitization is the process of pooling various types of contractual debt, such as mortgages, auto loans, or credit card debt obligations, and selling their related cash flows to third-party investors as securities. This transformation allows illiquid assets to be converted into marketable securities. The impact on credit risk is complex. It can reduce credit risk for the originating lender by transferring the risk to investors. However, it can increase systemic risk if the securitization process is poorly managed or understood, leading to excessive risk-taking and complex financial instruments that are difficult to value. The risk is dispersed, but the overall understanding and management of the underlying assets can become opaque, potentially exacerbating losses during economic downturns.

Specifically, securitization involves creating asset-backed securities (ABS). The originating lender sells the assets to a special purpose vehicle (SPV), which then issues securities backed by these assets. Investors receive payments from the cash flows generated by the underlying assets. The credit risk is then theoretically distributed among the investors holding the ABS. In a nutshell, it changes the way credit risk is held, which could have positive or negative impact.

10. How do you adjust credit risk assessments for qualitative factors not captured in financial statements?

To adjust credit risk assessments for qualitative factors, I would employ a combination of techniques. Firstly, conduct thorough due diligence focusing on management quality, industry trends, and the competitive landscape. This often involves gathering information from sources beyond financial statements such as industry reports, news articles, and direct communication with the company's management.

Secondly, incorporate subjective scoring or weighting systems. For example, assign scores to management's experience, brand reputation, or regulatory environment. These scores can then be integrated into the overall credit risk assessment model, either by adjusting the probability of default or loss given default. Scenario analysis is also valuable, particularly to assess the impact of potential adverse events not directly reflected in historical financials.

11. Explain the difference between a secured and unsecured loan and the implications for credit risk.

A secured loan is backed by an asset (collateral), such as a house (mortgage) or a car (auto loan). If the borrower defaults, the lender can seize the asset to recover losses. An unsecured loan, like a credit card or personal loan, isn't backed by collateral. If the borrower defaults, the lender's recourse is limited to legal action or collection agencies.

The credit risk implications are significant. Secured loans generally have lower interest rates because the lender's risk is reduced by the collateral. Unsecured loans carry higher interest rates to compensate for the increased risk to the lender. Defaulting on a secured loan can result in the loss of the asset, while defaulting on an unsecured loan primarily impacts the borrower's credit score and potential legal repercussions.

12. What are some of the challenges in assessing credit risk for cross-border transactions?

Assessing credit risk in cross-border transactions presents unique challenges compared to domestic lending. One significant hurdle is the lack of standardized financial reporting and legal frameworks. Different countries have varying accounting standards, making it difficult to accurately compare financial statements and assess the borrower's financial health. Furthermore, enforcing contracts and recovering assets in a foreign jurisdiction can be complex and time-consuming due to differences in legal systems and potential political instability.

Another challenge is the currency risk. Fluctuations in exchange rates can significantly impact the borrower's ability to repay the loan, especially if their revenues are primarily in a different currency than the loan currency. Furthermore, information asymmetry is often more pronounced in cross-border transactions. Obtaining reliable and up-to-date information about the borrower's credit history, industry conditions, and macroeconomic environment can be difficult, increasing the risk of adverse selection.

13. How do you monitor credit risk after a loan has been issued?

After a loan is issued, ongoing credit risk monitoring is crucial. We track several key indicators including: payment history (delinquency, defaults), changes in the borrower's credit score and credit utilization, and any significant life events that could impact repayment ability (e.g., job loss, divorce, public records). External factors such as industry trends and economic conditions are also monitored for potential impact.

Specifically, this involves regularly reviewing financial statements if available, tracking news and events related to the borrower or their industry, and using statistical models to predict potential defaults. If warning signs are detected, we may proactively reach out to the borrower to offer support or explore options for restructuring the loan.

14. Describe the different types of credit derivatives and their uses.

Credit derivatives are financial contracts whose value is derived from the credit risk of an underlying asset, such as a bond, loan, or portfolio of loans. Common types include: Credit Default Swaps (CDS), which are like insurance against default; Total Return Swaps (TRS), where one party pays the total return of an asset and receives a fixed or floating rate; and Collateralized Debt Obligations (CDOs), which are securities backed by a pool of debt obligations.

They are used for various purposes, including hedging credit risk (protecting against losses due to default), speculation (profiting from changes in credit spreads), and arbitrage (exploiting price differences in the market). For example, a bank might use a CDS to hedge the risk of a loan it has made, or an investor might use a TRS to gain exposure to an asset without owning it directly.

15. How do you handle a situation where a borrower is showing early signs of financial distress?

When a borrower shows early signs of financial distress, I proactively reach out to understand the situation and explore potential solutions. This involves reviewing their loan terms, current financial standing, and any specific challenges they are facing. I'd explore options such as:

- Payment Plans: Offer temporary reduced payment options.

- Loan Modification: Adjusting loan terms (interest rate, term length) to make payments more manageable.

- Refinancing: Exploring options for a new loan with better terms, if applicable.

- Forbearance/Deferment: Temporarily pausing or reducing payments (with interest accruing).

The goal is to work collaboratively with the borrower to find a sustainable solution that prevents default while minimizing losses for the lender.

16. Explain the concept of credit scoring and its limitations.

Credit scoring is a statistical analysis used by lenders to determine the creditworthiness of individuals or businesses. It involves evaluating various factors, such as payment history, outstanding debt, credit history length, types of credit used, and new credit, to predict the likelihood of repayment. A numerical score, typically ranging from 300 to 850, is assigned, with higher scores indicating lower credit risk. Lenders use this score to decide whether to approve loans, set interest rates, and determine credit limits.

Limitations include: over-reliance on past behavior (may not reflect current circumstances), potential for bias (demographic factors could inadvertently lead to discrimination), inaccuracies in credit reports (errors can negatively impact scores), and limited scope (doesn't capture all aspects of financial stability, like assets). Also, it may not accurately predict the creditworthiness of individuals with limited credit history ('credit invisibles').

17. What are the key considerations when setting credit limits for a customer?

When setting credit limits, consider several factors to balance risk and customer needs. Key considerations include the customer's credit history (payment history, existing debt), their ability to repay (income, cash flow), and the nature of the business relationship (length of relationship, payment frequency). Also, the overall economic climate and industry-specific risks should be factored in.

Other important factors involve internal policies and risk tolerance. Setting limits too low can stifle growth, while setting them too high increases default risk. Regular reviews and adjustments to credit limits are necessary based on changes in the customer's financial situation and market conditions.

18. Describe the Basel III accord and its impact on credit risk management.