Deferred compensation can be a powerful tool for attracting and retaining top talent. It's an agreement where a portion of an employee's pay is set aside to be paid out at a later date, often retirement. This can be a great way to boost your employer branding.

For recruiters, understanding deferred compensation is key to positioning your company as a forward-thinking employer. Let's break down the ins and outs of these plans, so you can effectively communicate their value to potential candidates.

Table of contents

What is Deferred Compensation?

Types of Deferred Compensation Plans

Benefits of Deferred Compensation

Downsides of Deferred Compensation

Deferred Compensation vs. Traditional Retirement Plans

Deferred Compensation: Key Takeaways for Recruiters

What is Deferred Compensation?

Deferred compensation is a financial arrangement where a portion of an employee's earnings is paid out at a later date. This can include various forms, such as pensions, retirement plans, and stock options, allowing employees to plan for future financial security.

Employers offer deferred compensation as an incentive to retain employees over the long term. By tying compensation to future performance or tenure, companies aim to align employee interests with organizational goals, fostering loyalty and commitment.

Deferred compensation can be a powerful tool in recruitment, especially for senior positions. It provides a competitive edge by offering potential candidates a tangible stake in the company's future success, enhancing the overall employer value proposition.

Understanding the tax implications is crucial for both employers and employees when dealing with deferred compensation. Depending on the structure, deferred earnings may be taxed differently, impacting the net benefit for employees and the financial planning strategy for companies.

For HR professionals, effectively communicating the benefits and intricacies of deferred compensation during the recruitment process is essential. Clear explanations help candidates appreciate the long-term value and align their career objectives with the company's offerings.

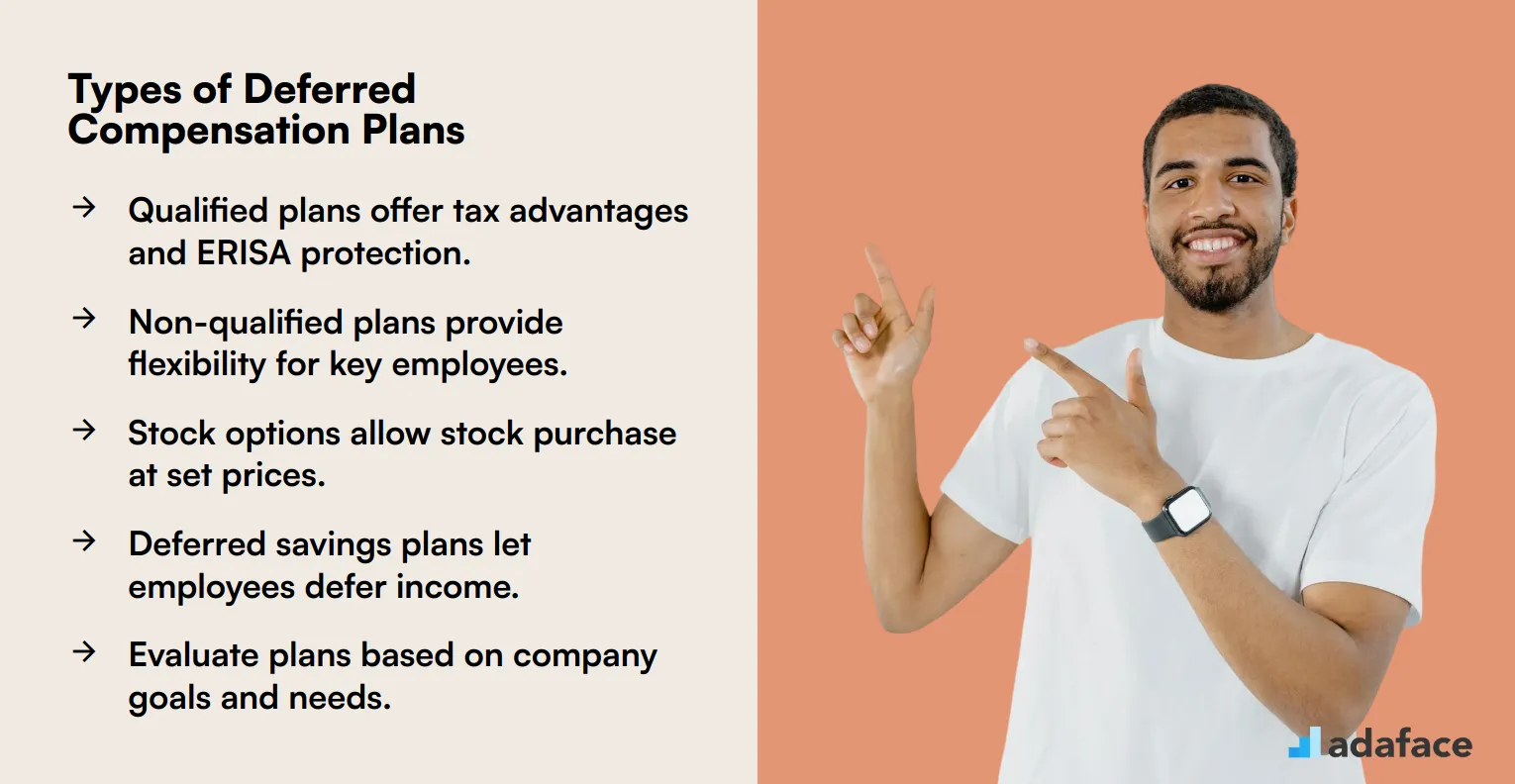

Types of Deferred Compensation Plans

Deferred compensation plans come in various forms, each designed to meet different financial goals and employee needs. The two main categories are qualified and non-qualified plans, each with distinct tax implications and regulatory requirements.

Qualified plans, such as 401(k)s and pension plans, are governed by ERISA and offer tax advantages to both employers and employees. These plans typically have contribution limits and non-discrimination rules to ensure fair treatment across all employee levels.

Non-qualified plans, including executive bonus plans and supplemental executive retirement plans, offer more flexibility but lack the same tax benefits as qualified plans. They are often used to provide additional compensation to key employees or executives beyond what's allowed in qualified plans.

Other types include stock options, which give employees the right to purchase company stock at a predetermined price, and deferred savings plans, where employees can defer a portion of their salary or bonuses. Each plan type has its own set of rules, benefits, and considerations that employers must carefully evaluate.

Understanding these different types of deferred compensation plans is crucial for recruiters and HR professionals to effectively communicate benefits packages to potential hires. It's important to consider the company's goals, employee demographics, and financial capabilities when selecting and implementing these plans.

Benefits of Deferred Compensation

Deferred compensation offers several benefits for both employers and employees. For employers, it serves as a tool to attract and retain top talent without immediately impacting cash flow. Employees, on the other hand, can enjoy tax advantages by deferring income to a later date when they might be in a lower tax bracket.

Another advantage is that deferred compensation plans can be tailored to meet the specific needs of high-level executives or key personnel. This flexibility allows companies to create customized packages that align with their talent acquisition strategies. Moreover, such plans can foster a sense of loyalty and commitment among employees, as they are incentivized to stay longer to reap the benefits.

Deferred compensation can also serve as a financial planning tool for employees, helping them manage their future retirement needs. By deferring a portion of their salary, they can potentially reduce their taxable income in the present, leading to more efficient financial management. This can be particularly appealing for those in high-income brackets looking to optimize their long-term financial health.

For recruiters and hiring managers, understanding the benefits of deferred compensation can be a valuable asset in negotiations. It allows them to offer competitive packages that go beyond immediate salary, appealing to candidates' long-term career and financial goals. This knowledge can enhance their recruitment strategies and contribute to building a more attractive employer brand.

Downsides of Deferred Compensation

Deferred compensation can be a double-edged sword for employees, particularly due to its inherent complexities and potential risks. One significant downside is the lack of immediate access to funds, which can be a concern in case of unforeseen financial needs or emergencies.

Another issue is the uncertain nature of future payouts, which are often contingent on the company's performance and financial health. Employees might find themselves at a disadvantage if the company faces financial difficulties or goes bankrupt, potentially losing their deferred earnings.

Tax implications can also be a drawback, as deferred compensation is typically taxed at the time of distribution, which might coincide with a higher tax bracket for the employee. This could result in a larger tax burden compared to receiving the income upfront.

Additionally, deferred compensation plans can sometimes be perceived as complex and difficult to understand, leading to potential misunderstandings or mismanagement by employees. This complexity might deter some individuals from opting for deferred compensation, especially if they prioritize immediate financial stability over long-term benefits.

Finally, deferred compensation can affect an employee's liquidity and flexibility, limiting their ability to invest or spend money as they see fit. This lack of control over their earnings might not align with the financial goals of all employees, making it a less attractive option for some.

Deferred Compensation vs. Traditional Retirement Plans

Deferred compensation and traditional retirement plans are both methods for saving for retirement, but they differ in structure and tax treatment. Deferred compensation plans allow employees to postpone receiving a portion of their income until a later date, often retirement, while traditional plans like 401(k)s offer immediate tax benefits.

One key difference is eligibility; deferred compensation is typically offered to high-level executives, while traditional plans are available to a broader range of employees. Deferred compensation plans also offer more flexibility in terms of contribution limits and distribution options, but they come with greater risk as the funds remain part of the company's assets.

Tax treatment is another significant distinction between these two types of plans. With traditional retirement plans, contributions are often made with pre-tax dollars, reducing current taxable income, while deferred compensation is usually taxed upon distribution.

Deferred compensation plans can be either qualified or non-qualified, with qualified plans subject to ERISA regulations and non-qualified plans offering more flexibility but less protection. Traditional retirement plans, on the other hand, are generally qualified plans that must adhere to specific IRS rules and contribution limits.

While both options can be valuable for retirement savings, the choice between deferred compensation and traditional plans depends on individual circumstances and financial goals. It's important for employees to carefully consider the pros and cons of each option before making a decision.

Deferred Compensation: Key Takeaways for Recruiters

Deferred compensation can be a powerful tool for attracting and retaining top talent, but it's also complex. As recruiters, understanding the basics is key to communicating these benefits effectively to candidates.

Think of deferred compensation as a delayed paycheck. Instead of receiving all their earnings now, employees agree to receive a portion of their compensation at a later date, often retirement.

For recruiters, understanding deferred compensation helps you explain the offer package clearly. It also allows you to position it as a valuable benefit that aligns with candidates' long-term financial goals, similar to understanding relocation package.

When discussing deferred compensation, highlight the potential tax advantages. Explain how deferring income can lower their current tax burden and potentially grow their savings over time.

Be prepared to answer questions about the plan's specifics. Candidates will want to know about vesting schedules, payout options, and any associated risks, so be ready to address them.

Conclusion

Deferred compensation plans offer a unique way for employers to attract and retain top talent. By understanding these plans, recruiters and HR professionals can better explain their value to potential hires and current employees.

While deferred compensation comes with both benefits and risks, it remains an important tool in the compensation toolkit. As with any financial decision, it's crucial for employees to carefully consider their personal circumstances and consult with financial advisors before participating in such plans.

For recruiters and hiring managers, being well-versed in deferred compensation can be a game-changer in negotiations. It allows you to present a more comprehensive compensation package, potentially giving your company an edge in the competitive talent market.

Deferred Compensation FAQs

What types of employees benefit most from deferred compensation?

High-income earners and executives often benefit most, as it allows them to defer taxes on current income. Employees nearing retirement may also find it attractive for long-term financial planning.

How does deferred compensation impact a company's talent acquisition strategy?

Offering deferred compensation can make a company more competitive in attracting top-tier candidates. It signals financial stability and a long-term investment in employees.

What are the key legal considerations for deferred compensation plans?

Plans must comply with IRS regulations, including rules on eligibility, vesting, and distribution. Consult with legal counsel to ensure compliance and avoid penalties.

How can recruiters explain the risks of deferred compensation to candidates?

Be transparent about the potential downsides, such as the risk of company insolvency or changes in tax laws. Emphasize the importance of diversification and seeking financial advice.

What role does candidate experience play when offering deferred compensation?

A positive candidate experience is crucial. Clearly communicate the details of the plan, answer questions thoroughly, and provide resources for candidates to make informed decisions.

How does deferred compensation compare to other benefits in terms of employee attraction?

Deferred compensation can be a significant differentiator, especially for attracting senior-level talent. It complements other benefits like health insurance and paid time off, creating a compelling overall package.

40 min skill tests.

No trick questions.

Accurate shortlisting.

We make it easy for you to find the best candidates in your pipeline with a 40 min skills test.

Try for freeRelated terms

Join 1200+ companies in 80+ countries.

Try the most candidate friendly skills assessment tool today.

40 min tests.

No trick questions.

Accurate shortlisting.

No trick questions.

Accurate shortlisting.